Multi-Country & Entity Group Health Insurance

Managing teams across multiple countries or entities? Discover your group health insurance options tailored to your global workforce—whether it’s one group health insurance policy, or tailored coverage for each location or something inbetween.

Watch the YouTube version or read the below article.

As businesses expand across borders, managing employee benefits like group health insurance becomes more complex. One of the key decisions business owners face is whether to opt for a single, global group health insurance policy or to implement separate policies for each country. Here’s a breakdown of both approaches to help you make an informed decision.

Option 1: One Global Group Health Insurance Policy

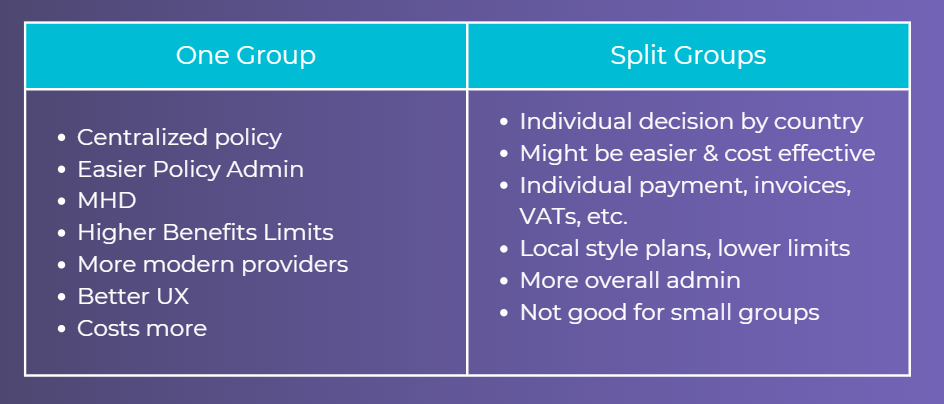

Many multinational companies choose to have a single group health insurance policy covering employees across multiple countries. Typically companies that do this are smaller in nature. This approach streamlines the process and offers several key advantages.

Pros:

- Easier Policy Administration: You bring things under one roof, one contract, create a consistent employee benefits package for all your employees. Having a single policy means fewer contracts to manage, fewer renewals, and a simpler relationship with one insurance provider. Your HR team(s) won’t have to juggle multiple policies, which can be a significant time-saver.

- Medical History Disregard (MHD): When you take on one global policy, you’re more likely to benefit from MHD. This means pre-existing medical conditions can be covered & waiting periods are waived. For international providers, this starts at 10 employees or adults. By grouping all your employees from different countries together, it’s easier to achieve this.

- Better Claims Experience: by having MHD, it means claims processes will be smoother as each individual employee does not have to go through full medical underwriting. Because of this, the insurer does not have to assess whether a claim is a pre-existing condition or not.

- Better User Experience: Not all providers allow employees to live across mulitple countries, the ones that do, generally speaking, are more modern, higher benefit limits, better technology & have the best direct billing networks.

Cons:

- Higher Cost: While one global policy streamlines many aspects of insurance management, it generally comes at a premium. Larger group policies may cost more because they often cover more comprehensive benefits and have higher administrative costs.

- Limited Flexibility: Different countries may have different healthcare needs, and a one-size-fits-all approach may not suit local practices or regulations.

Option 2: Separate Country-Specific Group Health Insurance Policies

Another approach is to manage separate group health insurance policies for each country where you operate. This can be a more decentralized but flexible method.

Pros:

- Lower Cost: By working with local providers, you can often access more competitive rates that reflect the cost of healthcare in each specific country. Additionally, you’re not paying a premium for the global administrative and service support that international insurers may offer.

- Financial Flexibility: From a Profit & Loss (P&L) or accounting perspective, separating policies by country can make it easier to manage costs at a local level. This may be particularly important for businesses that operate as distinct regional entities where you want to pay from each entity & get any invoice, VATs, etc.

Cons:

- Loss of Group Discounts: When you divide employees into separate, smaller groups, you lose the bargaining power that comes with larger group policies. This can lead to higher premiums or fewer benefits for employees.

- More Administrative Work: Managing multiple policies across different countries means dealing with a variety of insurers, contracts, and renewal dates. This adds complexity to your HR and administrative workload.

- No Consistency Across Countries: Your employees may have vastly different healthcare experiences depending on their location. This lack of cohesiveness in employee benefits can impact their perception of your company’s overall benefits package.

- Full Medical Underwriting for Small Groups: If you have only a few employees in certain countries, local insurers may require full medical underwriting, which could lead to exclusions for pre-existing conditions or other limitations.

Option 3: Semi-Split Groups

This method would particularly apply if you have entities in high-cost countries like Hong Kong or Singapore, where the cost of a health insurance premium would be cost prohibtive for the employees who are in cheaper countries like Vietnam, Cambodia, Thailand, etc.

With this style, you could:

- Create 1 group for Hong Kong/Singapore

- Create 1 group for employees in other countries

Summary

If your company is considering reviewing your current group plan or exploring options for the first time, we’d be happy to assist.

We can provide expert guidance and develop a customized proposal comparing the most suitable providers for your needs.